- Effective March 2026

Prevent ACH Payout Fraud: How the 2026 Nacha Rule Changes Payment Verification

The 2026 Nacha rule requires organizations sending ACH payments to strengthen fraud monitoring. Here’s what the change means, who it affects, and how payment teams can reduce risk before funds are sent.

2026 Nacha Rule: What You Need to Know

Who It Applies To

Non-consumer originators and third-party service providers originating ACH payments.

What Changed

Must implement risk-based processes to detect potentially fraudulent entries.

Key Dates

Implemented in two phases beginning March 20, 2026 and June 19, 2026.

What to Review

How you detect suspicious payment activity and validate payment details.

Verifying bank account ownership before initiating payments can help reduce fraud risk, support stronger ACH controls, and strengthen compliance without creating avoidable workflow friction.

Why ACH Fraud Risk Is Increasing

ACH payments are widely used for payroll, vendor payments, insurance payouts, refunds, and marketplace disbursements. As ACH volumes continue to grow, fraud targeting these payment flows has increased as well.

Many fraud incidents occur when payments are sent to bank accounts that were never properly verified, often after account details are changed during vendor onboarding, payout setup, or payment updates. Because ACH payments are often automated and processed in batches, fraudulent changes may not be detected until after funds have already been sent.

Vendor Updates

Fraudsters impersonate vendors and request account changes.

Insurance Payouts

Payment instructions modified before disbursements are sent.

Platform Payouts

Fraudulent accounts added to receive marketplace funds.

Refunds & Rebates

Details submitted without confirming account ownership.

What the 2026 Nacha Rule Requires

Nacha governs the Automated Clearing House Network, which processes electronic payments

across the United States. Under the 2026 rule update, organizations must implement risk-based processes to identify and monitor potentially fraudulent ACH entries.

Monitoring Requirements

Processes must be designed to detect transactions that may be unauthorized, initiated under false pretenses, or associated with potential fraud. Organizations are expected to update these regularly.

Who is Affected

Applies broadly to organizations originating ACH transactions: businesses sending payments, financial institutions, third-party

processors, payroll providers, and

service platforms.

Implementation Timeline

Phase 1: March 20, 2026

For entities with >6M transactions in 2023.

Phase 2: June 19, 2026

Applies to all remaining

non-consumer originators.

How Companies Can Prepare

Does your current process flag suspicious account changes before the ACH file is generated and funds

are sent? Review these key areas of your payment operations.

Assess current fraud monitoring processes

Work with risk, compliance, and payment teams to evaluate how outgoing ACH transactions are currently monitored.

Review account validation procedures

Determine whether bank accounts receiving payments are validated before funds are sent.

Evaluate technology and integration requirements

Consider whether existing payment systems support stronger monitoring and validation processes.

Prepare internal teams

Educate finance, operations, and risk teams about updated requirements.

Verify bank account ownership before initiating payments

Confirm that the receiving account belongs to the intended recipient before sending funds.

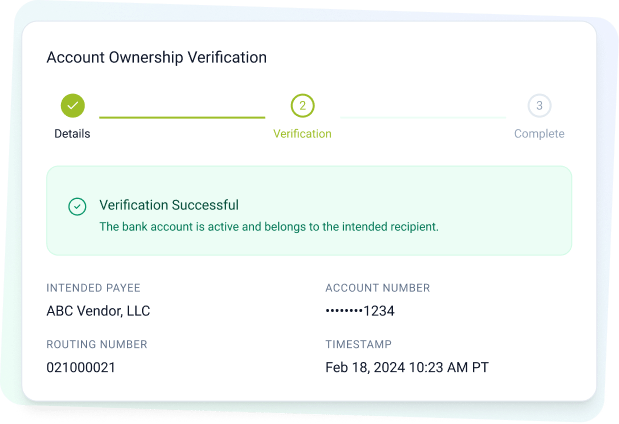

How Lyons Helps Verify Account Ownership Before Funds Are Sent

Lyons helps organizations verify bank account ownership before ACH payments are initiated. This helps teams confirm that the account belongs to the intended recipient before funds are sent, reducing fraud risk and strengthening payment controls.

- Verify bank account ownership before ACH payments are initiated

- Reduce exposure to fraudulent account changes

- Strengthen payment controls without adding unnecessary friction

Strengthen Payment Verification Before Funds Are Sent

Evaluate your monitoring and validation processes to reduce fraud exposure and stay ahead of compliance.